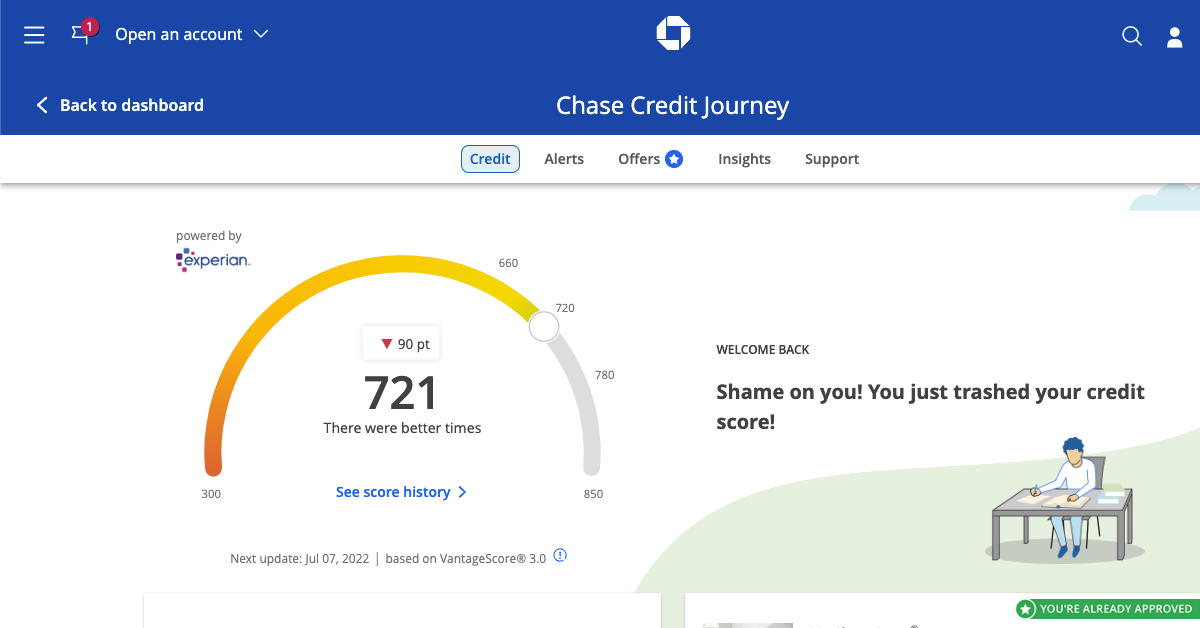

Credit Journey is a free credit score monitoring service from Chase bank. It provides a wide range of information like overall score, how many credit accounts you have, age of your credit, credit utilization, recent credit score inquiries, late payments etc. You may wonder if Credit Journey accurately shows your credit score.

There are 3 agencies that provide FICO credit scores to banks. These are TransUnion, Equifax, and Experian. Scores from each of these agencies can differ by a few points.

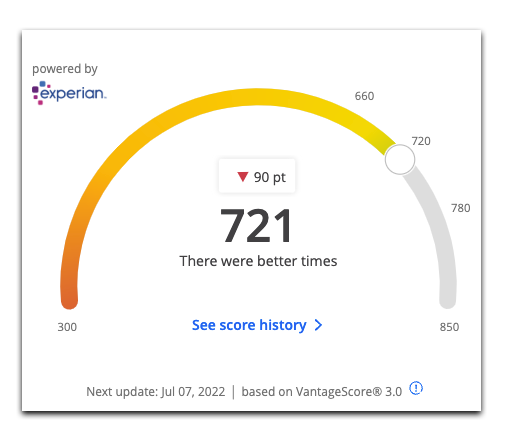

Chase uses the Experian version of credit score. It is VantageScore v.3. What I like in Credit Journey is that it updates credit scores weekly, while other credit tracking tools update their scores monthly. It means that most of the time the credit score from Credit Journey is more accurate than from others.

You should keep in mind, however, that credit scores presented in all credit score tracking tools are for education purposes. Often lenders receive their version of credit score. Credit card companies receive one version, when you apply for a mortgage bank receives another version. The likelihood that you will be approved or denied for a credit card is typically not affected by your exact score. So it doesn’t matter if your Credit Journey score is accurate. You may be turned down because of a high utilization rate or a high number of recent inquiries, but not because “your credit score is below 800 points.”

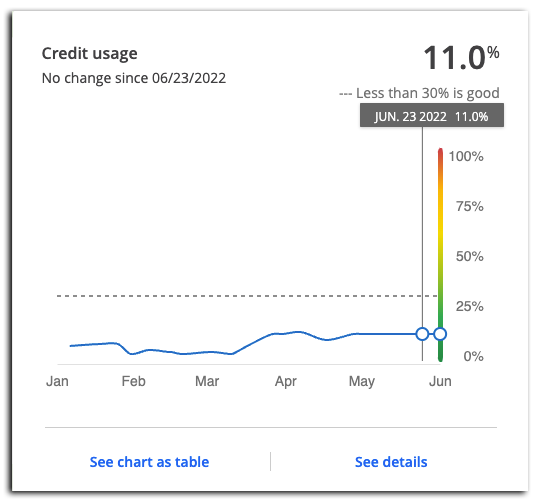

High credit utilization that Credit Journey presents is not always accurate. Its update can lag by a week. So when you pay off all your balances it can show high utilization for a few days. Therefore when you paid your credit card debt make sure to let this information to arrive in all credit bureaus. Otherwise it can seriously affect your odds of approval for a credit card, personal loan, auto loan, and mortgage. Accurate influence of this parameter from Credit Journey makes it a perfect way to quickly raise your chances.

Often credit education sites recommend you to keep utilization below 30%. However, my experience show that even an increase from 2% to 11% can drop credit score by 40 points.

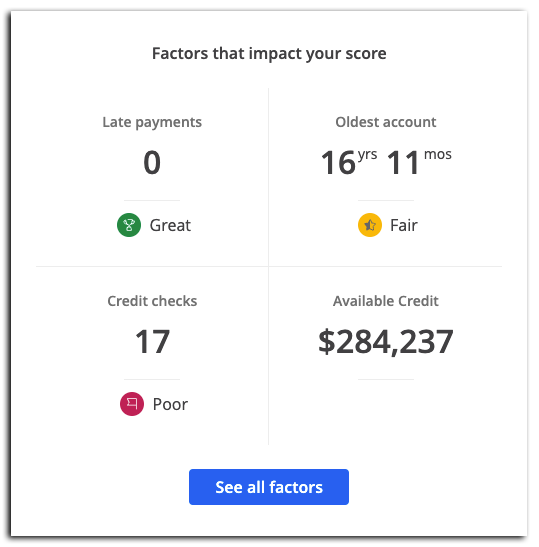

You should also keep in mind, that opening checking account doesn’t affect your credit score.